The state is pioneering an auto IRA for workers of small companies without 401(k) plans.

By Robb Mandelbaum

March 9, 2018, 8:00 AM EST - Bloomberg

Erick Marsh never expected to have a career. For six years after high school, he bounced from job to job at restaurants and food processors in Albany, Ore., never staying more than a year. Then at 24, he applied for an opening at an outpost of Del Taco, a chain based in Lake Forest, Calif. “I didn’t want to work fast food,” Marsh says. But with a baby on the way, he needed steady employment. Thirteen years later, he manages that same franchise and also works as the district manager for the family-run company that owns the franchise and four others along Oregon’s Interstate 5.

Despite landing stable employment, Marsh hadn’t planned for retirement. His employer, Cactus Enterprises LLC, decided a 401(k) program was too expensive to set up. And Marsh couldn’t bring himself to investigate the complex world of individual retirement accounts. “It’s one of these things I keep thinking to myself, I’ll do it next year, or I’ll do it next summer after the holiday, when I’m caught up with my bills.”

There are fewer excuses now for indecision in Oregon. Last July it became the first state to set up its own Roth IRA program for workers who don’t receive retirement benefits, providing them the option to make after-tax contributions to an investment account. Over the next two years, every employer in Oregon that doesn’t offer a retirement plan—a group that includes some 64,000 businesses and nonprofits, accounting for about 600,000 workers—must enroll their workers in the state-run IRA, known as OregonSaves. Employees can drop out of the plan any time after they’re enrolled.

Cactus Enterprises signed on last November, four months after the program was inaugurated. For Marsh, auto enrollment was the push he needed. “When it’s put right there in front of your face, it’s so much easier to say, ‘Yeah, let’s do this.’ ”

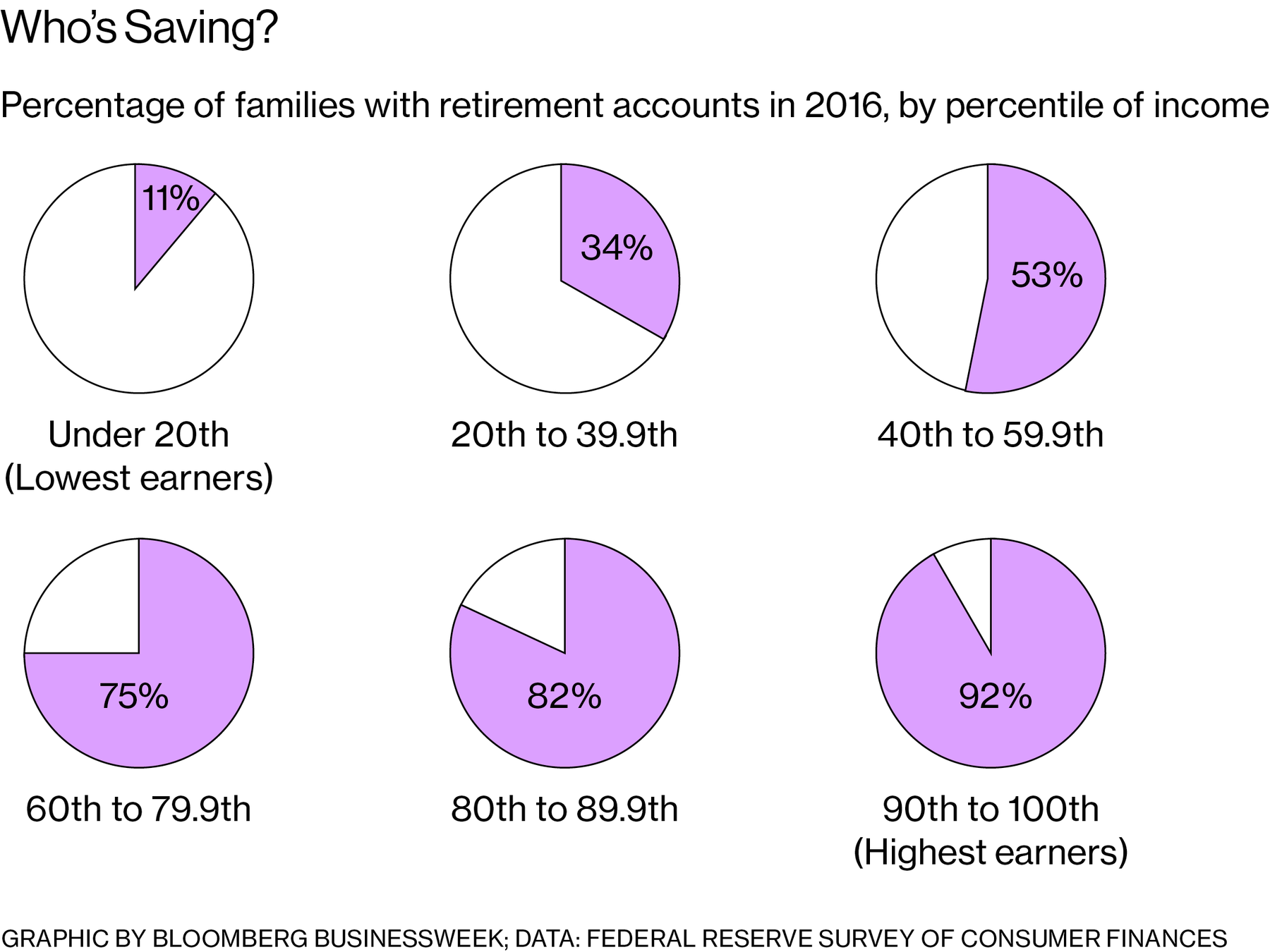

Contributions are now pouring in. The state treasurer’s office says enrollments have ballooned since December, from just more than 1,000 people to 27,000. The stakes are high. “Not enough people are saving enough for retirement,” says Tobias Read, who sponsored the OregonSaves law in 2015 as a state representative and now, as the state’s treasurer, is implementing it. “And when people don’t save for retirement, the already stretched state budget gets further stretched.” According to an analysis by AARP, which has advocated for auto IRAs, if lower-income retirees had an extra $1,000 in income each year, Oregon would save $100 million over the next 15 years in spending on social services for them. The savings for every state would amount to $8 billion and $33 billion for the federal government.

The potential for savings has elicited interest from other states. California—where 7.5 million workers don’t have access to a retirement savings account—and Illinois are starting their own pilot programs later this year. Two other states and Seattle have similar programs planned.

The key feature in the Oregon plan is the automatic enrollment. The inertia that beset Marsh is typical—people with workplace plans are 10 to 15 times more likely to save than those without, says David John, an AARP policy adviser who helped develop the model for OregonSaves. “When you have payroll deduction, you don’t think about it,” he says. The inertia works both ways. In Oregon about 80 percent of participants have stuck with the program, Read says.

OregonSaves’ default payroll deduction is set at 5 percent, though employees can choose any amount, as much as the Roth maximum ($5,500 a year for people under 50 for 2018). Each year the plan automatically increases the deduction by 1 percentage point, up to 10 percent. Employees can opt out of the increase, too.

Participants have three investment choices: a money-market fund, an index fund targeted to their retirement year, or a growth index fund. By default, the first $1,000 goes into the money-market account; everything after goes into a targeted fund. (Oregon has no say over the investments, which are managed by State Street Corp.)

Marsh is letting the plan do the thinking for him. “I haven’t really looked at it,” he says. “I just haven’t had time.” After-tax contributions to a Roth account can be withdrawn at any time without penalty, and at retirement age the investment proceeds aren’t taxed.

Companies contribute nothing to the IRA. Debbie Winnen, who owns Cactus Enterprises with her family, says OregonSaves costs her only some time—about two hours initially to register employees and about five minutes to 10 minutes each pay period for additional paperwork. Only 35 of her 110 workers have stayed in the plan. Most can’t afford the deduction, she says, but “the ones that are doing it, they love it.” These include her three children, who help run the business.

The requirement to register employees unsettled some local trade groups. “The bottom line is that businesses have been hit in the last couple years with a lot of increased rules and regulations and increased costs,” says Greg Astley, director of government affairs for the Oregon Restaurant & Lodging Association. But he says the state has worked to avoid creating a burden for employers. Nonetheless, the financial industry and the U.S. Chamber of Commerce have mobilized against auto enrollment, claiming, among other things, that the state programs don’t do enough to protect investors, an argument that puts the business lobbies in unfamiliar territory. They may be more worried, as the Chamber has argued, that state-run auto-IRAs might induce smaller companies to abandon their own plans. Last year the groups persuaded Republicans in Congress to overturn Obama-era rules that would have given these plans protection under federal labor law—a potential first step toward suing to shut them down.

Read acknowledges the program has limitations—for instance, the lack of an employer match. But, he says, OregonSaves has persuaded several companies to launch their own retirement plans. “We view that as a good outcome,” he says. For now he’s focused on expanding OregonSaves, first to self-employed people, who can sign up starting in December. Read says he hopes workers at companies that have retirement plans but are excluded from them can eventually join. He plans to add a traditional IRA next year and hopes to offer a socially responsible fund as an investment choice.

“The point is that everybody has access to a way to save for retirement at work,” he says, “and to build this culture of savings.”